The Sveriges Riksbank Prize in Economic Sciences in Memory of Alfred Nobel was established in 1968 by the Bank of Sweden, and it was first awarded in 1969, more than 60 years after the distribution of the first Nobel Prizes.

It has been awarded 51 times to 84 Laureates who have researched and tested dozens of ground-breaking ideas. Here are five prize-winning economic theories that you’ll want to be familiar with. These are ideas you’re likely to hear about in news stories because they apply to major aspects of our everyday lives.

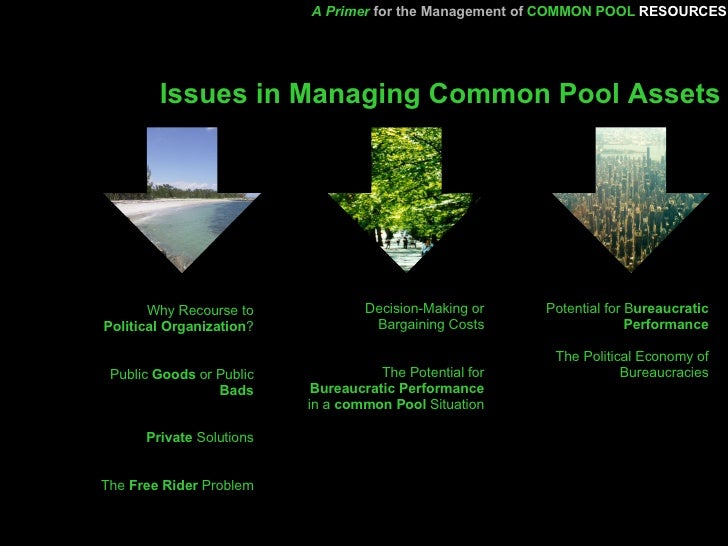

1. Management of Common Pool Resources

In 2009, Indiana University political science professor, Elinor Ostrom, became the first woman to win the Nobel Prize in economics. She received it “for her analysis of economic governance, especially the commons.

Management of common-pool resources is a resource that benefits a group of people, but which provides diminished benefits to everyone if each individual pursues his or her self-interest. The value of a common pool resource can be reduced through overuse because the supply of the resource is not unlimited, and using more than can be replenished can result in scarcity. Overuse of a common pool resource can lead to the tragedy of the commons problem.

2. Behavioral Economics

The US academic Richard Thaler won the Nobel prize in economics for his pioneering work in behavioural economics. The Royal Swedish Academy of Sciences, which awarded the £845,000 prize, praised Thaler for incorporating psychological assumptions into analyses of economic decision-making.

Unlike the field of classical economics, in which decision-making is entirely based on cold-headed logic, behavioural economics allows for irrational behaviour and attempts to understand why this may be the case. The concept can be applied in miniature to individual situations, or more broadly to encompass the wider actions of a society or trends in financial markets. The theory is particularly useful for companies and marketers looking to increase sales by encouraging changes in behaviour by consumers.

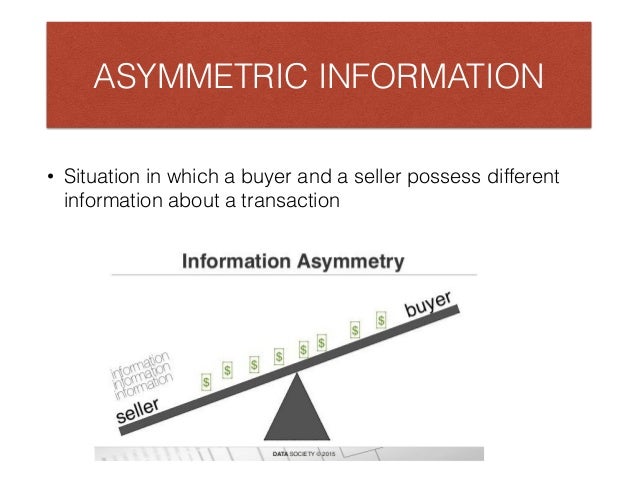

3. Asymmetric Information

In 2001, George A. Akerlof, A. Michael Spence, and Joseph E. Stiglitz won the prize for their analyses of markets with asymmetric information. The theory showed that economic models predicated on perfect information are often misguided because, in reality, one party to a transaction often has superior information, a phenomenon known as information asymmetry.

An understanding of information asymmetry has improved our understanding of how various types of markets work and the importance of corporate transparency. Asymmetric information can also be viewed as the specialization and division of knowledge, as applied to any economic trade. For example, doctors typically know more about medical practices than their patients. After all, physicians have extensive medical school educational backgrounds that their patients generally don’t have. This principle equally applies to architects, teachers, police officers, attorneys, engineers, fitness instructors, and other trained professionals. Asymmetric information, therefore, is most often beneficial to an economy and a society in increasing efficiency.

4. Game Theory

The academy awarded the 1994 prize to John C. Harsanyi, John F. Nash Jr., and Reinhard Selten for their pioneering analysis of equilibria in the theory of non-cooperative games. The theory of non-cooperative games is a branch of the analysis of strategic interaction commonly known as “game theory.”

One of Nash’s major contributions was the Nash Equilibrium, a method for predicting the outcome of non-cooperative games based on equilibrium. Nash’s 1950 doctoral dissertation, “Non-Cooperative Games,” details his theory. The Nash Equilibrium expanded upon earlier research on two-player, zero-sum games. Selten applied Nash’s findings to dynamic strategic interactions, and Harsanyi applied them to scenarios with incomplete information to help develop the field of information economics. Their contributions are widely used in economics, such as in the analysis of oligopoly and the theory of industrial organization, and have inspired new fields of research.

5. Public Choice Theory

James M. Buchanan Jr. received the prize in 1986 for his development of the contractual and constitutional bases for the theory of economic and political decision-making. Using Buchanan’s insights regarding the political process, human nature, and free markets.

He showed that contrary to the conventional wisdom that public-sector actors act in the public’s best interest as “public servants”, politicians and bureaucrats tend to act in their self-interest, just like the private sector. He described his theory as “politics without romance.” We can better understand the incentives that motivate political actors and better predict the results of political decision-making. We can then design fixed rules that are more likely to lead to desirable outcomes.

Hy we are on Patreon: https://www.patreon.com/pyoflife